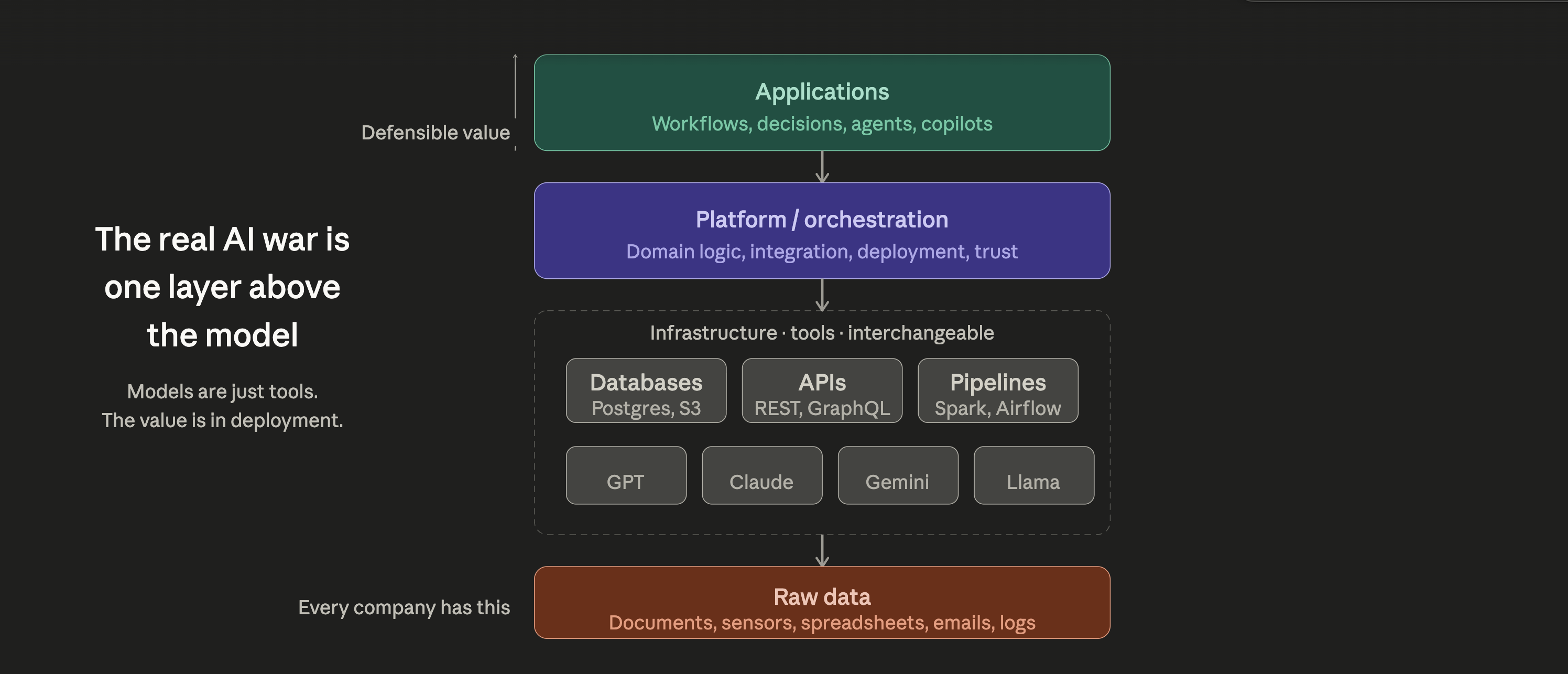

The Real AI War Is One Layer Above the Model

The AI War Isn't About Models Anymore

The model layer is becoming infrastructure → essential, commoditized, and low-margin. The value is migrating to the deployment layer: who can make these models actually work in the real world, for specific problems, inside specific organizations. The companies that figure this out will capture the next decade of value.

There's a pattern playing out in AI right now that most people outside the industry are missing. Everyone's watching the model race — GPT vs Claude vs Gemini vs Llama — but that race is already converging. The real battle has quietly moved up the stack.

LLMs are commoditizing. Fast.

The foundational models are going to converge toward parity. Each new release from any major lab closes the gap with the others within weeks. The architecture is largely shared, the research is increasingly open, and the talent pool rotates between the same handful of companies. We're heading toward a world where the base model is table stakes — necessary but not differentiating.

This is a textbook fast-follower dynamic. The first movers (OpenAI) bore the enormous cost of proving the market: the R&D, the infrastructure, the public evangelism. But once the path is proven, followers replicate the core capability at a fraction of the cost. Meta ships Llama for free. Mistral builds competitive models with a team a tenth the size. The pioneering investment doesn't create a durable moat when the underlying technology diffuses this quickly.

The unit economics problem no one talks about

OpenAI reportedly has north of 400 million users. At that scale, even a marginal loss per user (fractions of a dollar) compounds into billions in burn. They're not selling software at that point; they're subsidizing adoption and hoping to figure out monetization later. The fundraising isn't a sign of strength, it's the cost of staying alive while the model layer remains unprofitable at scale. They're essentially selling dollar bills for 90 cents and trying to make it up on volume, which, as the old joke goes, doesn't work.

The pivot up the stack

This is why you're seeing both OpenAI and Anthropic move aggressively beyond the base model. Claude Code. OpenAI's personal finance tools. These aren't side projects, they're the strategy. The model becomes the engine; the product is the specific solution built on top.

But the two companies are executing this transition very differently.

Anthropic is playing the enterprise game and playing it well

Anthropic has made a deliberate bet on the private sector. Rather than chasing consumer scale, they're embedding their products directly into enterprise workflows. You can see this in their hiring: they're aggressively recruiting Forward Deployed Engineers, poaching experienced FDEs from established players, and offering top-of-market compensation to do it. This isn't a hiring spree — it's a strategic land grab for the people who know how to make AI (or any other internal tool) work inside complex organizations from problem scoping to deployment to long-term adoption.

This is the right move, because this is where the defensible value lives. Getting an LLM to generate text is a solved problem. Getting an LLM to operate reliably within a Fortune 500's data environment, compliance requirements, and existing tooling is where the moat is.

This puts them in direct competition with the existing enterprise (AI) players

Here's what makes this interesting: by moving up the stack into enterprise deployment, Anthropic is now competing directly with companies like Palantir, Databricks, and Accenture's AI practice — firms that have spent years building exactly this layer. These companies sell integration, trust, and domain expertise, not models. And now Anthropic is showing up at the same table with a model advantage and a growing deployment capability.

Anthropic is doing this more effectively than OpenAI, which remains spread thin between consumer products, an API business, a hardware ambition, and an ongoing identity crisis about its corporate structure. Anthropic is more focused and more deliberate about where they compete.

The bottom line

The AI industry is repricing in real time. The model layer is becoming infrastructure → essential, commoditized, and low-margin. The value is migrating to the deployment layer: who can make these models actually work in the real world, for specific problems, inside specific organizations. The companies that figure this out, whether they started as model builders or enterprise integrators, will capture the next decade of value. The ones still racing to build a marginally better chatbot will find themselves in a margin squeeze they can't fundraise their way out of.